Amid easing geopolitical tensions and a rebound in Gulf markets following the halt of attacks between Iran and Israel, investors are cautiously optimistic about the opportunities in the region. In this environment, dividend stocks like ENBD REIT (CEIC) offer potential stability and income, making them an attractive consideration for those seeking to navigate market volatility with a focus on steady returns.

Top 10 Dividend Stocks In The Middle East

| Name | Dividend Yield | Dividend Rating |

| Yeni Gimat Gayrimenkul Yatirim Ortakligi (IBSE:YGGYO) | 3.23% | ★★★★★☆ |

| Turkiye Garanti Bankasi (IBSE:GARAN) | 3.37% | ★★★★★☆ |

| National General Insurance (P.J.S.C.) (DFM:NGI) | 7.89% | ★★★★★☆ |

| Matrix IT (TASE:MTRX) | 3.99% | ★★★★★☆ |

| Emirates Insurance Company P.J.S.C (ADX:EIC) | 8.31% | ★★★★★★ |

| Emaar Properties PJSC (DFM:EMAAR) | 8.91% | ★★★★★☆ |

| Dubai Insurance Company (P.S.C.) (DFM:DIN) | 5.88% | ★★★★★☆ |

| Arab National Bank (SASE:1080) | 6.19% | ★★★★★☆ |

| Anadolu Hayat Emeklilik Anonim Sirketi (IBSE:ANHYT) | 7.93% | ★★★★★☆ |

| Akbank T.A.S (IBSE:AKBNK) | 3.28% | ★★★★★☆ |

Click here to see the full list of 62 stocks from our Top Middle Eastern Dividend Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: ENBD REIT (CEIC) PLC is a Sharia-compliant real estate investment trust with a market cap of $125 million.

Operations: ENBD REIT (CEIC) PLC generates revenue primarily from its commercial real estate segment, amounting to $37.70 million.

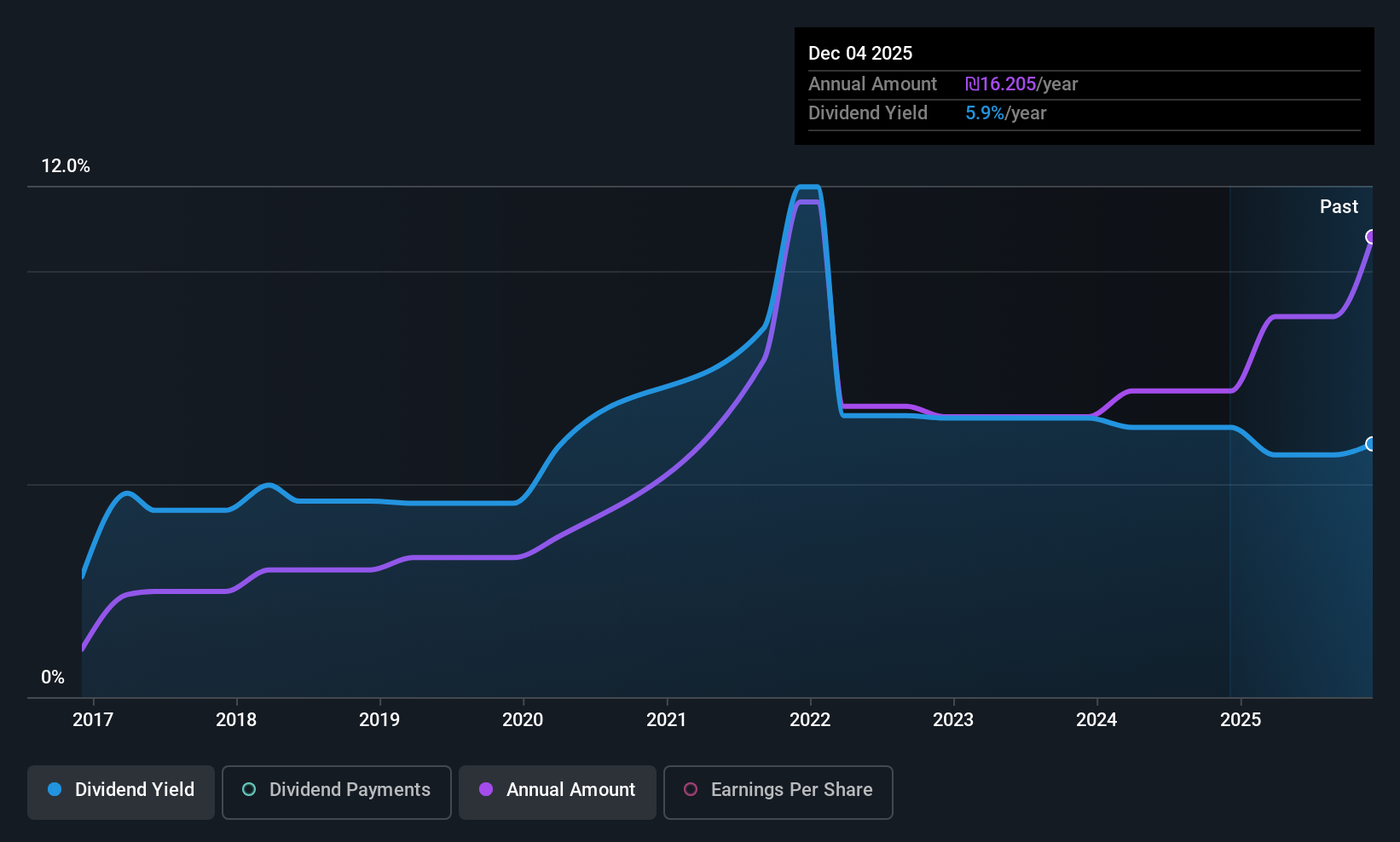

Dividend Yield: 8.2%

ENBD REIT’s recent earnings report shows a net income increase to US$45.5 million, indicating strong profitability. The dividend yield of 8.16% ranks in the top 25% within the AE market, supported by a cash payout ratio of 42.5%, suggesting dividends are well-covered by cash flows. However, the dividend track record is unstable with volatility over nine years and an overall decline in payments, highlighting potential risks for dividend consistency despite current coverage levels.

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: F.I.B.I. Holdings Ltd serves as the holding entity for The First International Bank of Israel Ltd, with a market capitalization of ₪10.37 billion.

Operations: F.I.B.I. Holdings Ltd’s revenue segments are not specified in the provided text.

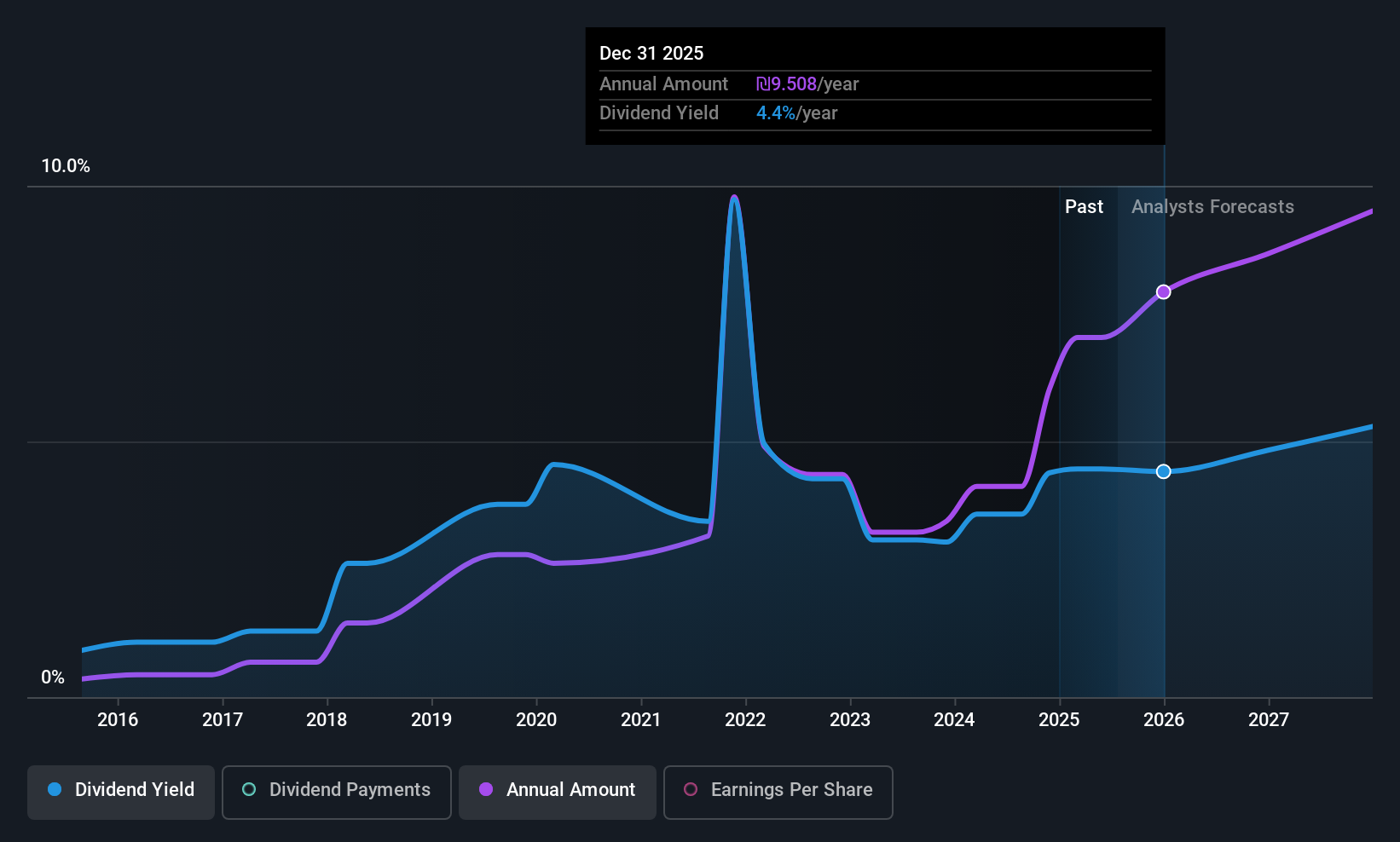

Dividend Yield: 5.5%

F.I.B.I. Holdings’ dividend yield of 5.54% is among the top 25% in the Israeli market, though its dividends have been volatile over the past decade with significant annual drops. Despite this volatility, a reasonable payout ratio of 53.9% indicates dividends are covered by earnings. The company’s recent earnings report shows a decrease in net income to ILS 231 million for Q1 2026 compared to ILS 255 million last year, which may affect future dividend stability.

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Mizrahi Tefahot Bank Ltd., along with its subsidiaries, offers a range of banking services both in Israel and internationally, with a market cap of ₪53.27 billion.

Operations: Mizrahi Tefahot Bank Ltd. generates revenue through several segments, including Operations in Israel – Others (₪3.08 billion), Private Banking (₪500 million), Large Businesses (₪1.83 billion), Medium Businesses (₪897 million), Residential Mortgages (₪4.46 billion), Institutional Investors (₪399 million), and Small and Micro Businesses (₪3.07 billion).

Dividend Yield: 5%

Mizrahi Tefahot Bank’s recent earnings report shows a slight decline in net income to ILS 1.24 billion for Q1 2026. The bank trades at 27% below estimated fair value, suggesting potential upside. Despite a low payout ratio of 50%, dividends have been unreliable and volatile over the past decade, with significant annual drops. Its current dividend yield of 5.05% is lower than top-tier payers in Israel, yet dividends are well-covered by earnings projections.

Seize The Opportunity

Interested In Other Possibilities?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment