As European markets show cautious optimism amid geopolitical developments and economic adjustments, investors are increasingly focused on identifying growth opportunities with strong fundamentals. In this context, companies with high insider ownership often attract attention as they may indicate a strong alignment of interests between management and shareholders, potentially offering resilience in uncertain market conditions.

Top 10 Growth Companies With High Insider Ownership In Europe

| Name | Insider Ownership | Earnings Growth |

| VIGO Photonics (WSE:VGO) | 20.8% | 84.6% |

| KebNi (OM:KEBNI B) | 11.8% | 82.7% |

| Hacksaw (OM:HACK) | 13.2% | 24.8% |

| Dellia Group (OB:DELIA) | 29.9% | 47.6% |

| CTT Systems (OM:CTT) | 17.5% | 47.1% |

| Clavister Holding AB (publ.) (OM:CLAV) | 18% | 83.1% |

| Circus (XTRA:CA1) | 21.9% | 84.4% |

| CD Projekt (WSE:CDR) | 35.2% | 26.9% |

| Bonesupport Holding (OM:BONEX) | 10.6% | 33.8% |

| Bergen Carbon Solutions (OB:BCS) | 11.9% | 50.2% |

Let’s explore several standout options from the results in the screener.

Simply Wall St Growth Rating: ★★★★☆☆

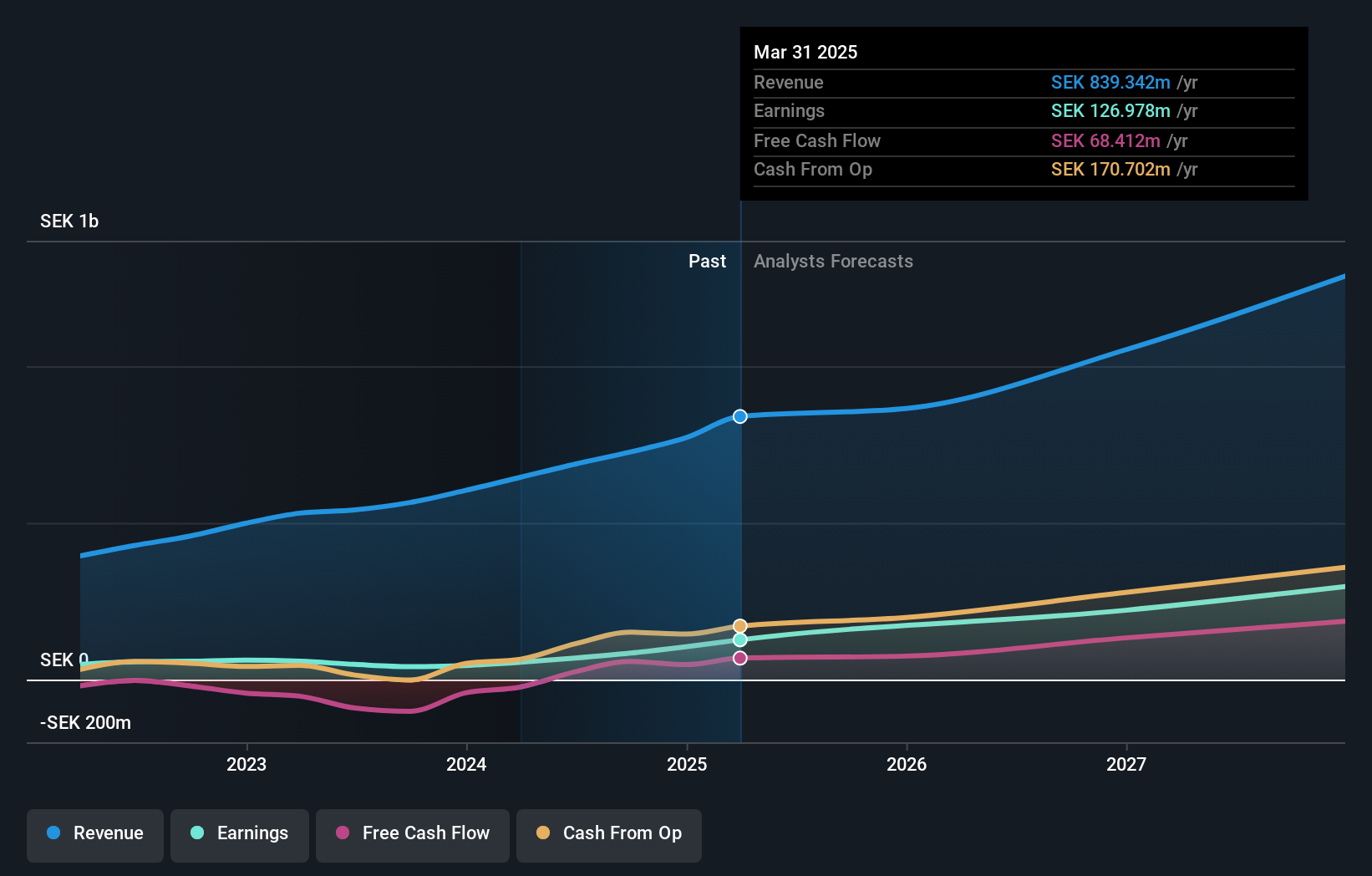

Overview: Plejd AB (publ) is a technology company that develops products and services for smart lighting, heating, and window covering across several countries including Sweden, Norway, Finland, the Netherlands, Germany, and internationally with a market cap of €12.29 billion.

Operations: The company’s revenue primarily comes from its Electronic Security Devices segment, which generated SEK 1.13 billion.

Insider Ownership: 39.1%

Revenue Growth Forecast: 19.9% p.a.

Plejd demonstrates characteristics of a growth company with high insider ownership, evidenced by its strong earnings growth of 38.1% annually over the past five years and projected earnings increase of nearly 30% per year, outpacing the German market. Recent first-quarter results show significant revenue and net income improvements, with sales reaching SEK 337.12 million from SEK 246.36 million last year, indicating robust operational performance despite no substantial recent insider buying activity.

Simply Wall St Growth Rating: ★★★★☆☆

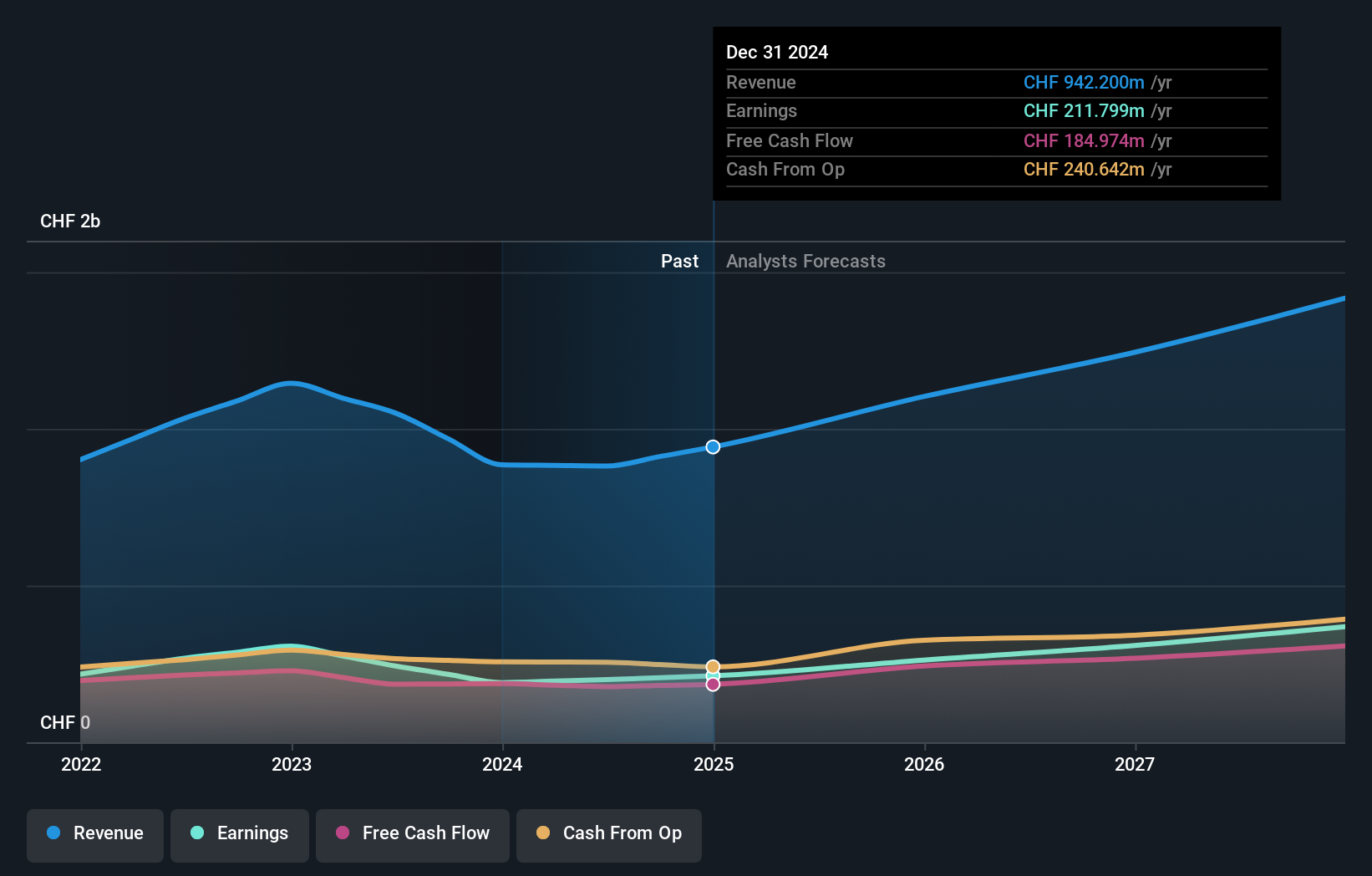

Overview: VAT Group AG, with a market cap of CHF18.72 billion, is involved in the development, manufacture, and sale of vacuum and gas inlet valves, multi-valve modules, motion components, and edge-welded metal bellows through its subsidiaries.

Operations: The company’s revenue is primarily derived from its Valves segment at CHF951.83 million and its Global Service segment contributing CHF198.85 million.

Insider Ownership: 10.2%

Revenue Growth Forecast: 13.6% p.a.

VAT Group shows potential as a growth stock with high insider ownership, forecasting earnings growth of 19.2% per year, outpacing the Swiss market. Despite recent executive changes and geopolitical challenges impacting supply chains, VAT remains resilient due to its global manufacturing footprint. The company anticipates higher sales and net income for 2026 compared to 2025, supported by strong demand in the semiconductor sector. However, no significant recent insider trading activity has been reported.

Simply Wall St Growth Rating: ★★★★☆☆

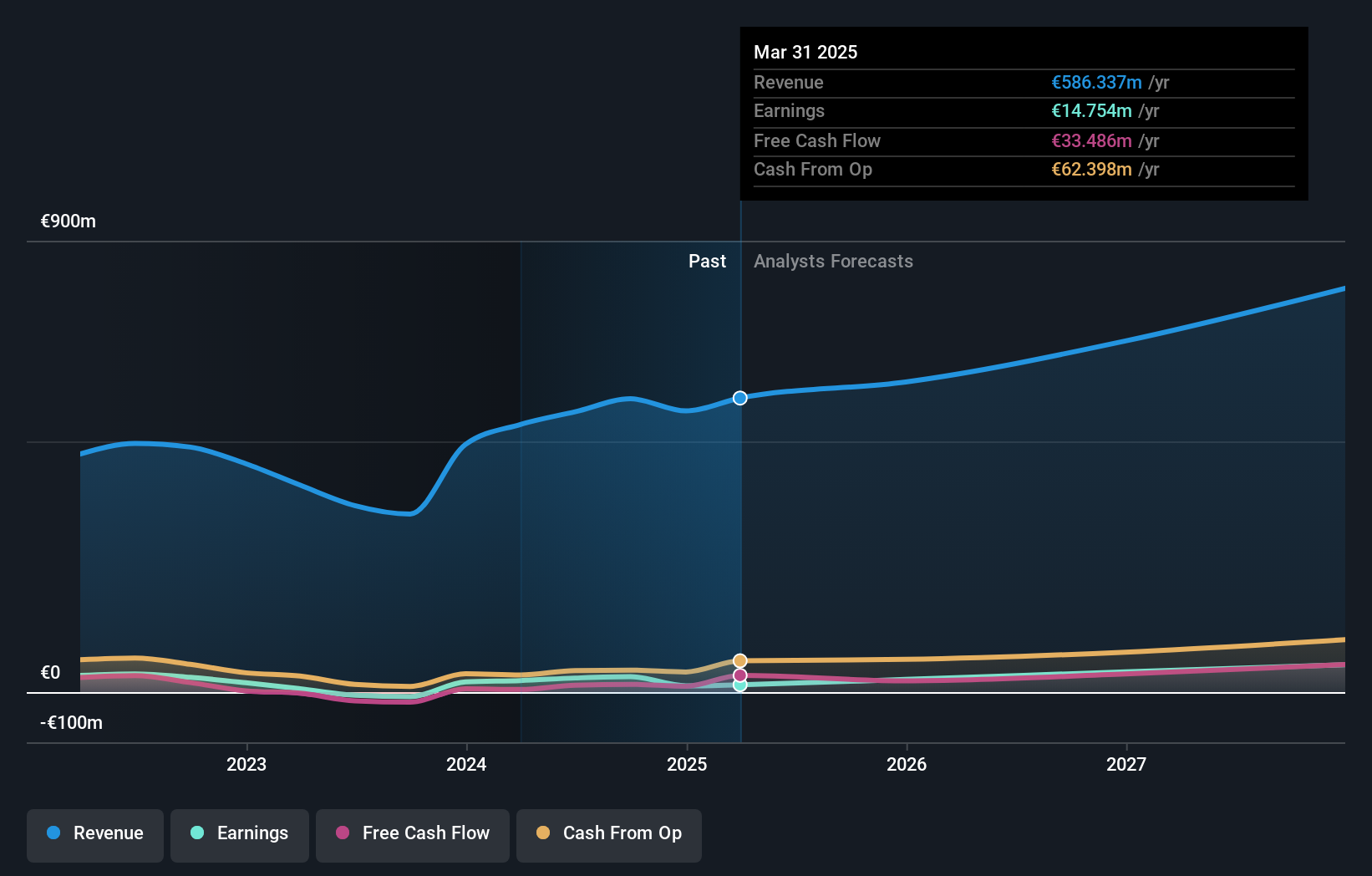

Overview: Hypoport SE develops, operates, and markets technology platforms for the credit, housing, and insurance industries in Germany with a market cap of €549.02 million.

Operations: The company’s revenue segments are comprised of technology platforms for credit services (€245.00 million), housing industry solutions (€365.00 million), and insurance-related offerings (€145.00 million) in Germany.

Insider Ownership: 33.5%

Revenue Growth Forecast: 10.3% p.a.

Hypoport demonstrates potential as a growth company with high insider ownership, with earnings expected to grow significantly at 24.1% annually, surpassing the German market’s growth rate. Despite volatile share prices and no recent significant insider trading activity, Hypoport’s revenue is projected to expand faster than the market at 10.3% per year. Recent earnings reports show improved performance, with Q1 sales reaching €169.27 million and net income rising to €7.82 million from the previous year.

Seize The Opportunity

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment