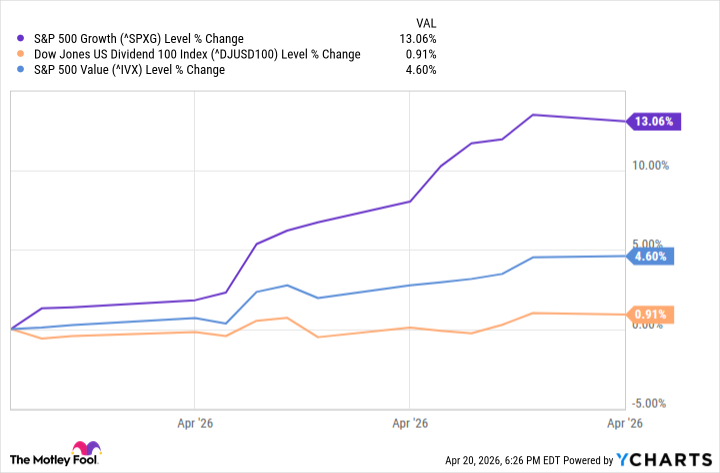

It’s been tough being an income investor of late. All the excitement seems to be on growth’s side of the fence. Indeed, after an alarming pullback in February and March, the S&P 500 Growth index is up nearly 13% just since the end of last month.

That seems to have come at the expense of value stocks, and at the expense of dividend stocks in particular. If income is your investing priority, though, this recent movement doesn’t change anything — other than perhaps reopening the door to an entry opportunity you might have missed.

With that as the backdrop, here’s a rundown of four of the market’s top dividend-paying prospects right now. Even if you’re already holding one or more of them, don’t rule out the idea of adding to an existing position.

1. Illinois Tool Works

Illinois Tool Works (ITW +1.90%) might be one of the stock market’s best-kept secrets.

Although its forward-looking dividend yield of 2.4% is far from thrilling, this company has been able to raises its per-share payout every year for the past 62 years — and by more than a little. Over the course of just the past 10 years, the stock’s quarterly per-share payment has improved from $0.55 to $1.61. That’s an annualized growth rate of more than 11%. A healthy cadence of stock buybacks has also boosted per-share profitability and payouts during this stretch.

Credit the nature of its businesses, mostly: None of them are exactly high-growth. All are consistently profitable, though, and increasingly so. These lines of business include always-marketable goods like industrial fluids, food-service equipment, welding supplies, car parts, and testing equipment.

Today’s Change

(1.90%) $5.08

Current Price

$272.17

Key Data Points

Market Cap

$77B

Day’s Range

$268.53 – $274.00

52wk Range

$228.76 – $303.15

Volume

22K

Avg Vol

1.4M

Gross Margin

43.60%

Dividend Yield

2.37%

2. Oneok

It’s been a wild ride for most oil stocks since the conflict in the Middle East materialized in early March. The disruption of supply chains creates scarcity, and scarcity raises prices. Most investors have spent the last couple of months guessing as to when matters might return to normal.

The one thing that scarcity and subsequently higher oil prices don’t do, however, is reduce the consumption of gasoline or diesel fuel — or for that matter, oil itself. The U.S. Energy Information Administration reports we’re still using just as much as we ever have, regardless of its cost.

While this might create cost and profit havoc for the companies drilling and refining oil, it doesn’t impact those simply transporting it from point A to point B. These are pipeline companies like Oneok (OKE +0.63%), which simply charges a fee for the amount of product it pushes through its pipes, regardless of the cost of the commodity traveling within their gas and oil delivery networks. This business is ideally suited for supporting recurring dividends.

Today’s Change

(0.63%) $0.54

Current Price

$86.60

Key Data Points

Market Cap

$54B

Day’s Range

$85.83 – $86.89

52wk Range

$64.02 – $95.30

Volume

1M

Avg Vol

5.1M

Gross Margin

18.31%

Dividend Yield

4.83%

Oneok is one of the best for income investors to consider right now. It’s currently offering a solid forward dividend yield of 5%, based on a payout that’s been not only reliable but also steadily growing for over a decade.

3. Verizon Communications

If you need your dividend stocks to also produce impressive capital gains and jaw-dropping dividend growth, you’ll probably end up disappointed in Verizon Communications (VZ +2.54%). On the other hand, with newcomers stepping into a forward-looking dividend yield of 6.1%, the lack of upside potential in these other metrics may still be well worth it.

Image source: Getty Images.

The core argument for owning Verizon as an income investment is clear. When money is tight, consumers might postpone the purchase of a new automobile, or do a little less shopping. But they’re unlikely to let go of their connection to the rest of the world; people will continue paying their mobile phone bills regardless of the cost.

The telecom giant has upped its payout for 19 consecutive years now. There are certainly other dividend payers out there with longer-lived growth pedigrees. Given that the company in its current form is only 26 years old, though, that’s actually a pretty solid streak. Verizon is also only a few years away from becoming dividend royalty, and as such is highly incentivized to ensure it keeps paying and growing its dividend.

4. Brookfield Asset Management

Finally, add Brookfield Asset Management (BAM 2.29%) to your list of dividend stocks to buy, or to buy more of even if you happen to already own some.

Just as the name suggests, Brookfield is an investment manager — a business with lots of competition. This one is unusual in that it doesn’t bother with the usual index-based or sector-themed mutual funds or exchange-traded funds (ETFs). Rather, it only manages a small handful of publicly traded funds, under its own name, that limit their focus to infrastructure (like data centers, pipelines, and railroads), or renewable energy businesses (like hydroelectric power, wind, and solar).

Brookfield Asset Management

Today’s Change

(-2.29%) $-1.11

Current Price

$47.40

Key Data Points

Market Cap

$79B

Day’s Range

$47.40 – $48.45

52wk Range

$42.20 – $64.10

Volume

48K

Avg Vol

4.1M

Gross Margin

96.43%

Dividend Yield

3.74%

While some might see this narrow focus as self-limiting, it’s actually brilliant; it doesn’t waste time, resources, or capital on businesses that aren’t positioned to offer as much return on investment. Instead, it devotes resources to the best growth opportunities for the near term and the foreseeable future.

And the company isn’t shy about touting its potential. It publicly says it’s looking for growth of between 15% and 20% per year, and adds that right around 90% of whatever profits it produces will be passed along to shareholders in the form of dividends. You’d be stepping into a solid dividend yield of around 4%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment